A prepaid debit card stores money and can be used for purchases. The card requires you to pay upfront to access the stored money. But you can continue to use it by reloading money onto it over time.

It’s one of the most recommended options for anyone struggling to manage their expenses. It’s also ideal for parents trying to limit their children’s finance and help them build financial responsibility.

Although they are generally costlier to manage, they offer some unique benefits. The cards are readily available and don’t often require rigorous processes to get. You can easily live a debt-free life when you use prepaid cards.

5 Best Prepaid Debit Cards in August 2026

The market is open, meaning no card issuer dominates the market share, though companies like Walmart, MasterCard, Amex, and Visa hold large shares. But, with many promising options out there, choosing one cannot be very clear. Moreover, each offer has advantages and disadvantages that can prove difficult to separate. Luckily, here is a curated list of the five best prepaid cards you can get in August 2026.

These are robust options suitable for various users, depending on your needs. While compiling this list, we considered important features such as ATM withdrawal fees, availability, monthly fees, etc. So, ensure you pay attention to all the features, details, and hidden fees to make a beneficial decision and apply for the right option.

|

Best Card Offers |

ATM withdrawals |

Reward |

Monthly Charges |

Cash Reloads |

|

Bluebird by American Express |

$2.5 on non-MoneyPass ATMs |

None |

None |

$0 |

|

American Express Serve FREE Reloads |

$2.25 service fee |

1% Cashback |

$6.95 for nonresidents of Texas, New York, and Vermont |

$0 |

|

Walmart MoneyCard |

$2.50 service fee |

3% cash back for purchases on Walmart online store. 2% at fuel stations and 1% at stores owned by Walmart (up to $75 annually). |

$0 with a deposit of $500+ monthly. But you’ll have to pay $5.94 for monthly deposits below $500 |

$3 fee at Walmart checkouts |

|

American Express Serve Cash Back |

$0 at MoneyPass ATMs. $2.5 charged at non-MoneyPass ATMs plus operator fee in some scenarios |

$0 |

$6.95 can be waived for $795 monthly purchases (no fee for NY, TX, and VT) |

Up to $3.95 (sometimes depends on the retailer) |

|

FamZoo Prepaid |

$0 |

None |

Up to $5.95 |

Up to $4.5 |

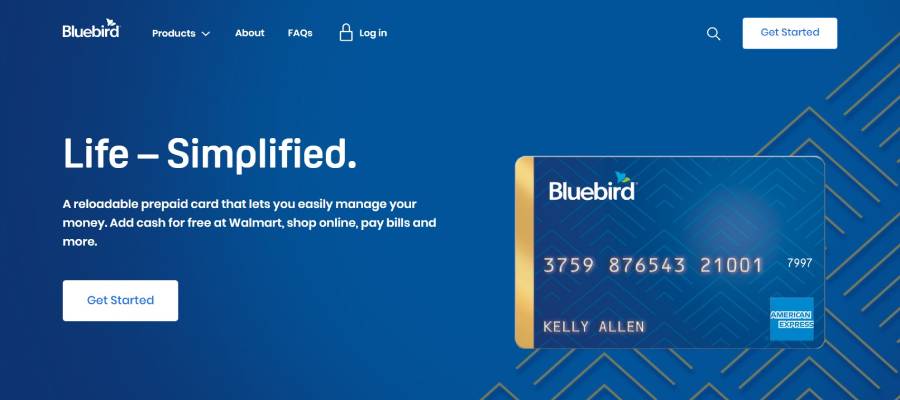

1. Bluebird by American Express

Bluebird by American Express allows you to access many traditional credit benefits without additional charges. Withdrawals at approved ATMs are free and international transactions won’t incur extra charges.

This card if best for

- Families that want dedicated kid accounts to practice saving.

- Anyone seeking a payment card with no overdraft or negative fee.

- People who can’t open a bank account or prefer low charges.

Highlights

ATM withdrawals: $2.5 on non-MoneyPass ATMs

Reward: None

Cash reload fee: $0

Pros of this card

- Users won’t be charged monthly or annually for transactions.

- Free withdrawals on extensive MoneyPass ATMs.

- Low balance alerts.

- Multiple options to fund your account.

Cons of this card

- No cashback offers on purchases and at retailers.

- Users often get charged for cash withdrawals.

- Not accepted everywhere, like Visa and MasterCard.

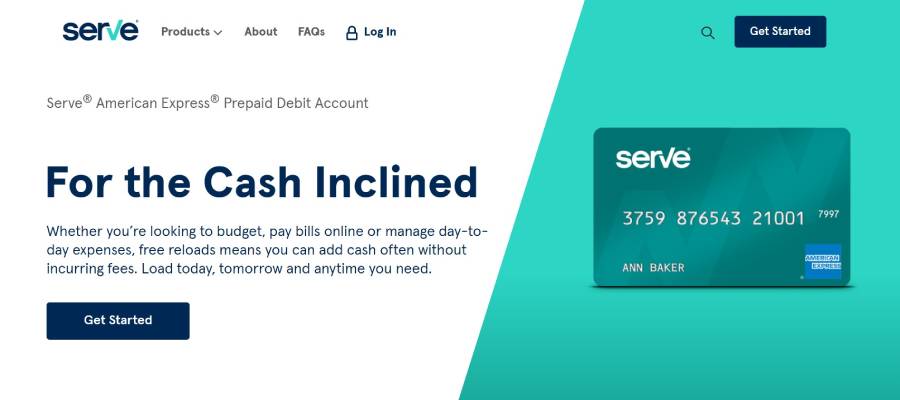

2. American Express Serve FREE Reloads

This has some impressive features for regular users. It is a solid option for anyone who reloads without expecting any fee. It is not conservative of monthly charges, though. It also doesn’t give the best rewards if that is what you seek.

This card if best for:

- Those who prefer traditional banking options, e.g., ATM access, direct and mobile deposits.

- Anyone who wants to develop better spending habits.

- People who don’t want to pay monthly or annual fees.

Highlights

ATM withdrawals: $2.25 service fee

Rewards: 1% Cashback

Monthly Fee: $6.95 for nonresidents of Texas, New York, and Vermont.

Cash Reload Fee: $0

Pros of this card

- Special service for disciplined and targeted saving goals.

- No monthly fees.

- Funding with many options.

- Incur $0 to load cash at retail locations nationwide.

Cons of this card

- A withdrawal fee of $2.5 on non-MoneyPass ATMs.

- No discount on foreign transaction charges.

- No reward rates for users.

3. Walmart MoneyCard

This option is one of the best for people who often purchase goods from Walmart store. Although Green Dot Bank issues them, you’ll get cashback rewards for all Walmart purchases you make. You’ll also get other free services.

This card if best for:

- People who have bad records on their bank accounts.

- Anyone who doesn’t mind loading $500+ monthly to reduce the monthly fee.

- Anyone who often buys goods at Walmart.

Highlights

ATM withdrawals: $2.50 service fee.

Rewards: 3% cash back for purchases on Walmart online store. 2% at fuel stations and 1% at stores owned by Walmart (up to $75 annually).

Monthly Fee: $0 with a deposit of $500+ monthly. But you’ll have to pay $5.94 for monthly deposits below $500.

Cash Reload Fee: $3 fee at Walmart retails.

Pros of this card

- Free cash reload and withdrawals across Walmart stores and its app.

- Free payments for all your online bills.

- Solid cashback rewards.

- Zero charges on direct deposits payroll and government benefits

Cons of this card

- Requires a $500 load to avoid a monthly fee.

- Charges ATM and bank teller a $2.50 fee.

- $3 fee for cash reloads at Walmart checkout.

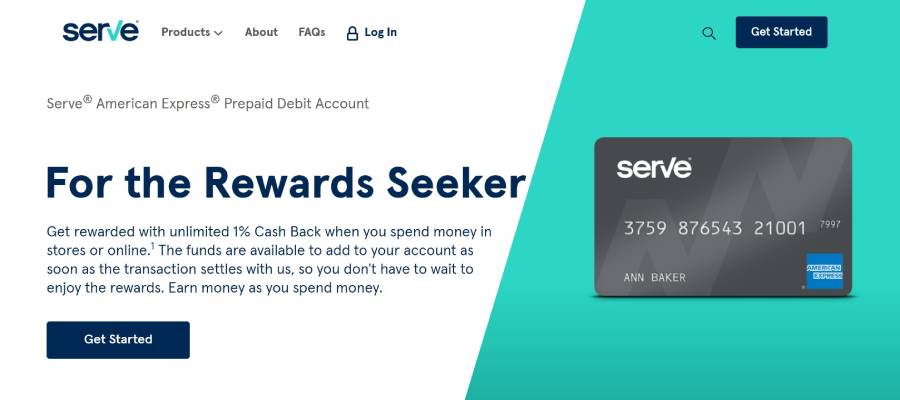

4. American Express Serve Cash Back

Although the unlimited cashback offer is regular, American Express Serve Cash Back is a good option. You can make free withdrawals across multiple ATM locations nationwide. You will also get waivers on multiple charges, such as deposits, card replacement, purchase protection, etc.

This card if best for:

- Anyone who doesn’t mind paying a $5.95 monthly fee.

- People who want purchase protection.

Highlights

ATM withdrawals: $0 at MoneyPass ATMs. $2.5 charged at non-MoneyPass ATMs plus operator fee in some scenarios.

Rewards: $0

Monthly fee: $6.95 can be waived for $795 monthly purchases (no fee for NY, TX, and VT)

Cash Reload fee: Up to $3.95 (sometimes depends on retailer)

Pros of this card

- Unlimited 1% cash back on purchases.

- Free withdrawals on more than 30,000 MoneyPass ATMs nationwide.

- Purchase protection on all eligible purchases.

Cons of this card

- Up to a $5.95 monthly fee.

- Pay up to $3.95 on cash reloads.

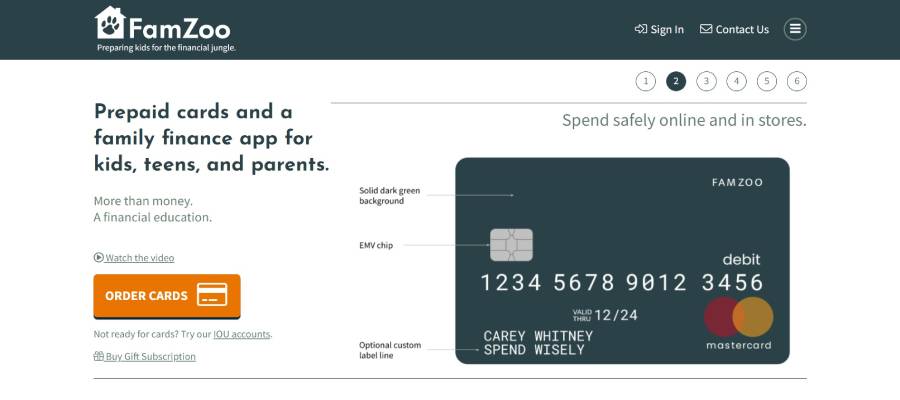

5. FamZoo Prepaid Debit Card

This option is the best bet for parents who want to share money and organize funds. It allows you to make swift payments and track all purchases. It’s perfect for developing healthy financial habits and creating incentives. In addition, users don’t get charged for the first month after they order.

This card if best for:

- Parents who want to manage their kids’ accounts and encourage them to save.

- Anyone who wants free nationwide ATM withdrawals.

Highlights

ATM withdrawals: $0

Rewards: None

Monthly fee: Up to $5.95

Cash Reload fee: Up to $4.5

Pros of this card

- Free cards for up to four requests.

- Free ATM withdrawals.

- Manage kids’ finance and allow them to save with parents’ interest.

- Multiple reload options, including Venmo, PopMoney, MasterCard rePower networks, etc.

Cons of this card

- Expensive monthly fee (can be reduced with advance pay).

- Up to $4.95 fee on cash reloads at retailers.

What Are Prepaid Debit Cards?

This is a plastic payment medium for purchases. It’s pre-valued, so you have to buy it with money already loaded. You can then use it for purchases up to the amount of money stored.

It’s sometimes called a stored-value card too. And it has some interesting features you don’t get on other alternatives. It’s a safer way to carry your funds around than a wad of cash.

This payment medium offers users some protection, e.g., insurance and purchase protection on all payments. You can use a prepaid card for mobile and online transactions with special benefits. Many users might prefer it as attractive gifts rather than cash.

Where Can I Get a Prepaid Card?

You can get a prepaid card from the issuer’s website, app, or retail stores. However, offers differ for each of them, so you need to narrow down to the ones that meet your demands. They often require you to pay an equivalent amount of money you want to store. But you can load additional funds onto it in various ways.

One of the easiest ways to add funds is through direct deposit into the intended account. It only requires a few details to do an electronic transfer from another bank account into yours. Otherwise, you can use MasterCard, ATMs, or mobile check deposits, which are similar to transfer deposits. This uses the camera on your phone to deposit checks. Lastly, you can make cash payments to a retailer who funds the account.

Pros and Cons of Prepaid Debit Cards

It all boils down to individual preference most times. But they do offer some advantages and disadvantages worthy of mention.

Pros

Easily accessible: You can easily get and use one anywhere without commitment to the issuer.

Safe: It is a denomination of your funds. So when you lose it or there’s a fraud, you’ll only lose a limited amount.

No bank account: You don’t need a bank account or link to a MasterCard account to get it.

No debt: Users won’t accumulate debt on their account, which helps keep healthy financial habits.

Overdraft and consumer protections: You can evade overdraft by stopping purchases at a $0 balance. Some issuers add various consumer protection policies, such as purchasing protection services.

Cons

Hidden fee: Most of them have hidden fees you’ll have to pay after purchase.

Less safe: It also has lesser purchases and fraud protection.

No impact on a credit profile: You won’t get credit reports from any credit bureau, so it doesn’t boost your score.

No interest policy: You probably won’t accrue interest on your stored funds.

How to Cancel a Prepaid Card?

The easiest way to cancel your card without the risk of losing your money is to withdraw all the funds. Of course, you must visit an ATM to do this and might even be charged a transaction fee. But it might be worth it in the long run.

You can also contact the issuer with details and the reason for cancellation. This might incur charges, so ensure you read the fine print before choosing the option. Some users might prefer getting rid of the available balance. To do this, purchase anything you won’t be returning and get rid of all the funds.

Prepaid Debit Cards vs. Regular Cards

Traditional or regular cards are linked to an existing checking or savings account. So, it serves as a medium to make payments from your account and usually has fewer downsides than its counterpart. You can also use it to receive any type of loan from a lender.

Meanwhile, a prepaid card allows you to store money and access it anytime. Unlike regular ones, you pay upfront rather than link to your bank account. As a result, you can continue to reload more money over time.

The card is good for budgeters and better funds management. Otherwise, there are more disadvantages compared to regular ones. For example, you can get hidden charges, limited purchases, ATM withdrawal charges, and inconvenient cash reload process.

Alternatives to a Prepaid Debit Card

If you don’t like prepaids, you have a few other options. Each has its advantages and disadvantages, so ensure you read about them. You can use money orders, cashier’s checks, and certified checks. A regular MasterCard is a good alternative if you have a bank account. It works similarly; the major difference is their source of funds.

You can also opt for a Credit Card though it has some different features. For example, rather than access available funds, you can access overdrafts on your account. You’ll then pay back the 500 dollar loan with bad credit to avoid lowering your credit score.

Conclusion

Prepaid cards are welcome nearly everywhere you can use a regular one. They are often issued or backed by a major bank or network like Amex or MasterCard. The downside is that they don’t help you grow your financial profile, you can only spend the amount you loaded on it, and the charges are often hefty.

They are good recommendations for anyone battling overspending and feeding up on using personal loans online same day deposit. Or parents trying to educate their kids on how to manage money. Some options, like Bluebird by American Express, offer exceptional services tailored to families. Hopefully, this guide will help you apply for a suitable option that meets your specific needs.

on your homescreen

on your homescreen